The Covid pandemic has led to a housing boom across the country, but in London demand has been relatively muted due to reduced migration as home buyers looked for more space outside the city.

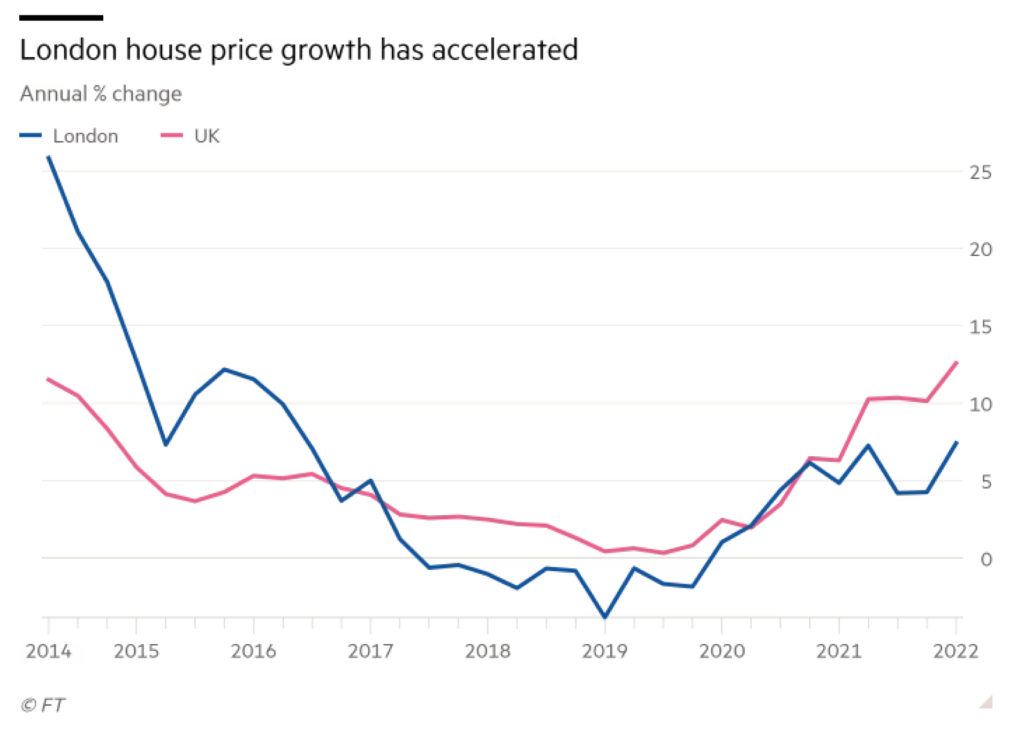

However, in the first quarter of this year, London house prices grew at an annual rate of 7.4 per cent, up from 4.8 per cent in the same period last year and the fastest rate since 2016, according to the mortgage provider Nationwide.

While the rate was still below the national average of 12.6 per cent, similar upward trends were reported in house prices compiled by Academetrics, Knight Frank and Halifax.

“The past two years have resulted in a loss of love for city centres such as London,” said Emma Cox, managing director of real estate at Shawbrook Bank.

“But as we see the city centre open their doors to businesses and hospitality… [these] hotspots once again are fast becoming an attractive place to be,” she added.

“Over the last few months, London has come back on the radar of buyers as the economy reopened,” said Tom Bill, head of UK residential research at Knight Frank.

The trend is echoed by other economic indicators. The average asking price of a London property up by an annual rate of more than 6 per cent, a reversal of the contraction that began in early 2021, according to the property website Rightmove.

The proportion of surveyors who expect house prices to rise in the capital was its highest since 2014, and greater than the national average for the first time since the crisis began, according to the Royal Institution of Chartered Surveyors, a professional body.

Rising demand has bumped against a shortage of London properties for sale. “The acute supply and demand imbalance across London has driven pricing and competitive bidding on properties,” said Angus Dixon, director of private clients at the property consultants INHOUS.

Activity is strongest among the most expensive properties where “buyers are less exposed to increased costs of living and costs of debt”, said Alec Harragin, a director at the London surveyor company Savills.

While John King, surveyor at Andrew Scott Robertson, confirmed that demand for houses in the £1mn-£2mn range “was the most active sector”.

Despite the pick-up, the London property market has been underperforming the national average since 2016 and still lags behind other regions in the UK.

A lack of foreign buyers still weighs on the capital’s housing market, according to Bill from Knight Frank, despite some improvements, adding that he expected it to underperform the national average in the months ahead.

Many experts warned that affordability was a longer lasting problem in the capital. Like the rest of the country, “concerns about interest rates, the economy and the war in Ukraine will be factors that could well dampen the market”, said Allan Fuller, of Allan Fuller Estate Agents in London.

Copyright The Financial Times Limited 2022. All rights reserved.

Full article – Financial Times – Valentina Romei (Subscription required)

Tenancy charges may vary, depending on the agreement we have with you, so it’s best to ask the INHOUS lettings department.

The following payments may apply when entering an Assured Shorthold Tenancy:

| First month’s rent | In advance |

| Tenancy Deposit | 5 weeks, or 6 weeks if annual rent is over £50,000 |

| Holding Deposit | One week’s rent, put towards your first rent due |

| Early termination when requested by the tenant | A charge not exceeding the financial loss experienced by the landlord |

| Default charge for late payment of rent | A maximum of 3% above Bank of England base rate, charged when rent is more than 14 days late |

| Default charge for replacement of lost key or security device | Equivalent to cost incurred |

| Changing the tenancy documents after the commencement of the tenancy, including change of sharer | £50 incl. VAT |

The following payments may apply when entering a Non-Housing Act Tenancy:

A Non-Housing Act Tenancy is formed when the annual rent exceeds £100,000 or the property is occupied by a Company rather that an individual.

| Inclusive of VAT | |

| Tenancy Setup Fee drafting and execution of tenancy agreement if supplied by us, collecting and holding the Security Deposit as Stakeholder, issuing protection certificates, if applicable, Open Banking type referencing of tenant and initial Right to Rent Checks | £360 |

| Check-in Fee checking into the property and reviewing inventory | minimum of £130 |

| Tenancy Continuation negotiating and drafting an extension | £150 |

| Change of Sharer – Deed of Assignment | £120 |

| Early Termination – Deed of Surrender | £120 |

| Guarantor Referencing Fee (each): | £30 |

| Deed of Guarantee Fee: | £50 |

| Late payment of rent | 3% above the Bank of England base rate |

This guide is for tenants and landlords in the private rented sector to help them understand their rights and responsibilities. This guide includes a checklist and further detail on each stage of the rental process.

Tenancy charges may vary, depending on the agreement we have with you, so it’s best to ask the INHOUS lettings department for a full breakdown of costs. Here’s a list of what you can typically expect to pay:

| Lettings Service Only: | 10%+VAT (12% inc. VAT) – Including rent collection |

| Letting and Management Service: | 16%+VAT (19.2% inc. VAT) |

| Short Let (less than 6 months): | 24%+VAT (28.8% inc. VAT) |

| Lettings Renewals Service: | 8%+VAT (9.6% inc. VAT) |

| Lettings and Management Renewal: | 14%+VAT (16.8% inc. VAT) |

| Short Let Renewal (less than 6 months): | 24%+VAT (28.8% inc. VAT) |

Additional non-optional fees and charges

We will not be charging clients fees for referencing, tenancy agreements or deposit registration.

The costs of a clean, EPC, gas safety, EICR, PAT and inventory are set by third party suppliers and prices may vary. The below schedule is to give you an idea of what you would typically pay.

All fees stated are inclusive of VAT (calculated at 20%):

During the tenancy (if required

INHOUS is a member of and covered by the ARLA/Propertymark Client Money Protection (CMP) Scheme.

We are also a member of a redress scheme provided by The Property Ombudsman www.tpos.co.uk.